Personal Injury Attorney Gives Advice on What to Do and Not Do Regarding Car Accidents

A car accident in Florida can be very expensive if you are not properly insured. When you are in an accident that results in injuries, going it alone with insurance claims adjusters can also be extremely expensive. Here are 16 important tips regarding auto insurance and insurance claims in Florida:

1. You must carry no fault/PIP insurance in Florida if you are licensed to drive or have a car registered in the state, and spend more than 90 days a year in the state. This type of insurance is only designed to cover the basics, including up to $10,000 per person for injuries and lost wages. Almost all drivers should have supplemental insurance as below.

If you are involved in an accident and you are not currently insured, you may lose your license until such time as you pay significant money to the DMV to get it back.

2. You should carry uninsured motorist insurance – While there is a law requiring everyone in FL to have insurance, many do not. Adding a rider for uninsured motorist is very inexpensive and will cover your injuries in a case where the accident is not your fault.

3. Carry GAP Insurance. Gap insurance, more accurately called gap protection, covers the difference between what you owe on your car and how much the car is worth. For many drivers, a standard auto insurance policy provides enough protection to cover the cost of repairs or replacement if their car is damaged or stolen. However, if you total your car and the car’s actual cash value is lower than the amount you owe on your loan balance or lease, that difference, or “gap,” is not covered by insurance. Your insurance company won’t pay out more than the car is worth (before it was damaged) — so you will be responsible for paying that amount.

Gap protection is designed to cover this difference between auto value and auto loan. Before you pay for gap protection, though, consider how a gap occurs and how you can close it.

Often, borrowers find themselves “upside down” (owing more than the auto is worth) through a combination of factors, including:

• Taking out a loan with an extended term. A longer loan term not only means lower payments, it means you build equity in the vehicle much more slowly.

• Depreciation. All cars depreciate, but some lose value much more quickly than others. According to some estimates, certain cars lose as much as 30% of their value within the first three months.

• Putting little or no money down. If you finance all or nearly all the price of the car, you could be upside down as soon as you drive home, because a new car depreciates most at the moment it becomes “used.”

• Borrowing more than the purchase price. Borrowers who finance the tax, license, and registration, or extras such as service plans and extended warranties, will find themselves upside down before leaving the lot.

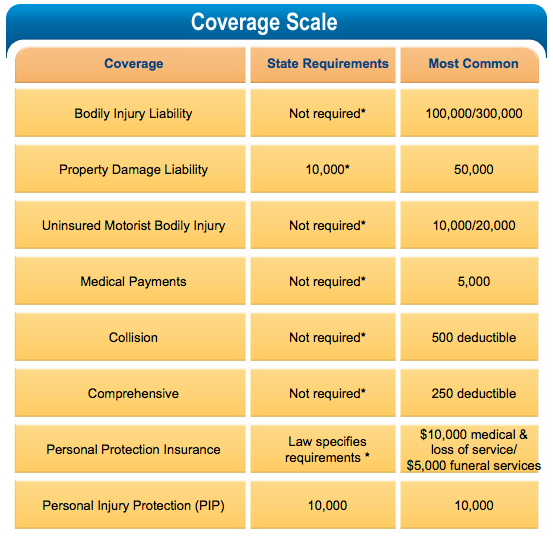

4. Purchase an insurance policy with higher coverage levels. Many cars today are worth $30,000 or more. Your minimum state required policy will not be enough to pay for damages to these types of automobiles. In addition personal injuries can commonly require payments well beyond the $10,000 PIP maximum coverage. For most individuals, you should be carrying a policy known as 100/300/50. This policy covers up to $100,000 in personal injury per person, $300,000 per accident, and $50,000 in property damage claims.

Below is a chart supplied by All-State which shows the average coverages for Florida. In addition to these coverage, high net worth individuals may want to add an umbrella to their homeowners insurance for $1,000,000 or more to cover all potential liabilities. This coverage is very inexpensive and could save you hundreds of thousands of dollars in the case of a serious accident.

After an accident, it is normal to be shook up and anxious. Take a few deep breaths and start with the obvious. Tend to anyone who is hurt. Make calls to 911 if necessary or to the relevant police agency if there are no injuries, but significant property damage or possible hidden injuries. To protect yourself and create the best chances for a future full recovery of any losses, do the following:

5. The Other Parties to the Accident: Do not apologize or explain anything to the other party or parties. Be kind and ask about injuries. Do not admit any aspect of fault. If they choose to make admissions, make a note of anything that they say. Make sure you secure their names, addresses, phone numbers, email, and insurance information. Use your phone to take pictures of their insurance card and accident damage.

6. Witnesses: If possible, talk to any witnesses. Take notes about what they saw. Get their contact information.

7. Take pictures and notes. Use your cell phone or other camera to take pictures of damages to all vehicles, various shots of the position of the cars at the scene before they are moved, and anything else related to the cause of the accident, such as a street light not working or construction issues. Now take careful notes of what you remember, and other aspects of the scene.

8. Police: Do not give police officers incriminating or other information that could show you to be at fault. You have no obligation to give the officer more than name, driver’s license, registration, and proof of insurance. Be careful. Even when the other driver is obviously totally at fault, your comments may accidentally provide evidence for the defense.

If the accident only involved minor property damage and no injuries, call your insurance company and they will help you through the process.

After an accident where you or parties in your car sustained injuries, follow these tips:

9. Call an attorney like Harris Gilbert or Andrew Smallman. They will help walk you through all the rest of these steps, and provide you with the best chance of a recovery that provides you with justice in your case.

10. If you have injuries, no matter how minor, see a physician for your injuries – don’t “tough it out!” Sometimes minor injuries have major consequences. The doctor may also see things that you don’t. The doctor bills and his analysis can be important evidence in generating just compensation for your injuries.

11. Never give a statement to the other driver’s insurance company before consulting a lawyer. No insurance company is your friend, but you can be doubly certain that the insurance company that is representing the other party to the accident is only looking out for themselves.

12. Do Not negotiate with the at fault drivers insurance company on your own. Sure, they’ve already admitted it was their fault. Now they just want to send you a settlement. They may seem like the nicest folks who are looking out for you. They aren’t. They are paid to do one thing. Keep the payout to you as low as possible. You need a trained negotiator to make that call.

13. Do Not settle your case without hiring an injury lawyer. Whether you are dealing with your own insurance company or the at fault driver’s insurer, everyone will be pushing you for a fast settlement. They know that the faster they settle, the less they will generally have to pay. They know that you are enticed by that check being dangled out as bait. They also know that sometimes, injuries take years to fully play themselves out. They want a settlement that eliminates any future payment for such surprises.

In some cases, the settlement check they send you will not be properly done, and you might even be open to liens and medical bill collections.

14. Don’t try to save a dime by not hiring a lawyer. That decision may cost you dollars and many headaches, backaches and neck aches later on! Research has shown that using a lawyer to help you in car accident injury claims results in a larger final payment to you, even after all legal fees. With the Law Offices of Gilbert and Smallman, you pay no fees or costs until you are paid by the insurance company. So there is no risk to you at all. And you avoid all the hassle and anxiety of dealing with the insurance company’s trained pit bull negotiators.

15. Tell your attorney everything – Do not hide anything. Tell the truth.

16. Even after hiring an attorney, never speak to the insurance company unless authorized by your lawyer. Call your attorney to give updates on doctors visits or other changes.

If you have been injured in a car accident in Miami, Hollywood, Fort Lauderdale or anywhere in South Florida, call us, Harris Gilbert or Andrew Smallman, on our personal cell phones: (786) 371-4431 or (954) 661-7371 any time 24/7!!